Governments are gently beginning to ease lockdowns, allowing economic activity and hope of a V-shaped recovery to continue. But a critical risk, for markets and society, is the risk of a ‘second wave’ of COVID-19 and subsequent government responses. Tightening or reimplementing lockdowns in this scenario will inevitably further damage economies.

Like a patient recovering from a general anaesthetic, time will be needed; something governments will be acutely aware of. As more data emerges, we begin to gain a clearer picture of the impact of the virus and different measures against it.

Here, we highlight 6 reasons why governments may, in fact, have reason to depart from the blunt instrument of a general nationwide lockdown and begin opting for a more localised approach. For patients and economies looking for a quicker recovery, this could be the answer

1) Lockdowns may not necessarily lead to fewer overall deaths

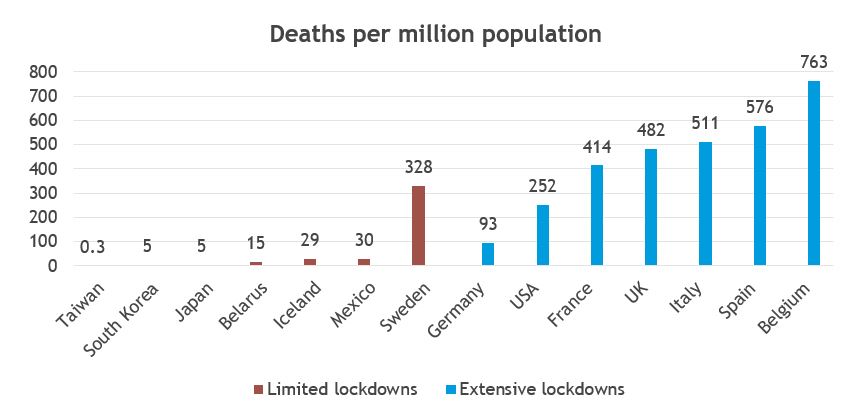

Governments have implemented varying degrees of lockdowns in response to the ongoing pandemic. Spain and Italy imposed some of the toughest restrictions in attempts to stem the number of deaths. Conversely, Sweden took a more laissez faire approach, limiting gatherings to 50 people. Currently, deaths per million people in Sweden sit at 328, lower than Italy, Spain and Belgium at 511, 576 and 763 respectively.1

Source: Worldometers/Smith & Williamson Investment Management LLP, as at 12 May 2020

Lockdowns are not futile, they increase social distancing, which slows the spread of disease. However, they are also not without cost. Nationwide lockdowns cause economic damage and may not necessarily lead to fewer overall deaths if it means significant delays in non-COVID-19 medical procedures (e.g. cancer screening, heart check-ups and visits to local GPs). If nationwide lockdowns are bottlenecking other medical issues for the future, then a more nuanced approach to assessing their effectiveness should be used.

A balance needs to be struck between lockdowns and their impacts on society. As more data emerges, governments could be less willing to enforce nationwide lockdowns a second time round, given the economic and possibly medical cost they come at.

2) Lifting lockdowns has not boosted COVID-19 cases in some countries

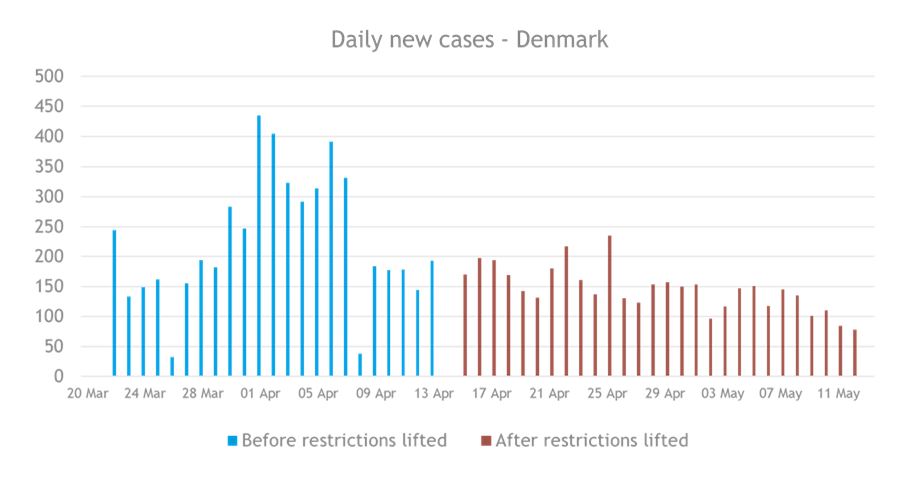

Denmark is the first Western country to reopen its elementary schools, leading the way out of lockdown. So far, the data indicates that lifting the lockdown did not equate to increased infections. COVID-19 cases in Denmark peaked in early April, slightly below 450 new cases a day. With the lockdown relaxed, new daily cases have continued to gradually decrease to 78 now, with notably less volatility than before2. If this trend continues and if it is representative of other countries, then there could be no need for re-imposed nationwide lockdowns.

Source: Bloomberg/Smith & Williamson Investment Management LLP, as at 12 May 2020

3) There may be social backlash against another nationwide lockdown

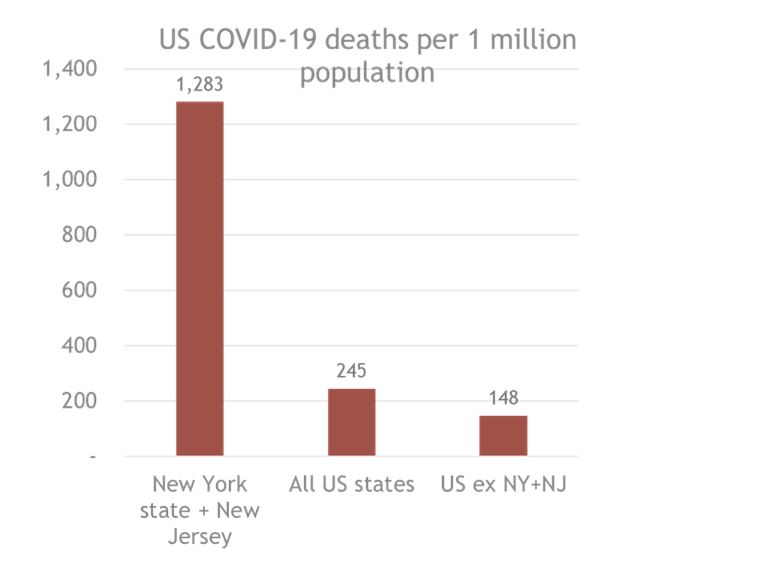

The link between population density and COVID-19 deaths can be seen clearly in the United States. New York state and New Jersey combined have 1,283 deaths per million people, whereas the US excluding them, has 1483. Population density and death rate correlations can be seen in Europe too. ‘Lived density’ is considered by some to be a more representative metric for population density, accounting for uninhabitable land and urban density, amongst other factors. Essentially it mitigates issues encountered when measuring countries such as Russia, where tightly populated cities are combined with vast sways of wasteland. It is unsurprising that of the ‘larger’ European countries, the 4 with the highest ‘lived density’ also have the highest deaths per capita4. Clearly, high density areas are structurally vulnerable to COVID-19 and may require continued lockdown.

However, residents in low density areas may begin to question why a national lockdown is necessary. Anti-lockdown protests have already begun in the US. Will residents in areas such as Montana continue to accept restrictions on their freedoms and, importantly, income when their area is largely unaffected? The potential social backlash to national lockdowns is a key risk for governments and especially in the US during an election year. Localised, targeted lockdowns could be a far more efficient and popular measure.

Source: Bloomberg/Smith & Williamson Investment Management LLP, as at 12 May 2020

4) Wearing facemasks could be a cheaper option to deal with COVID-19

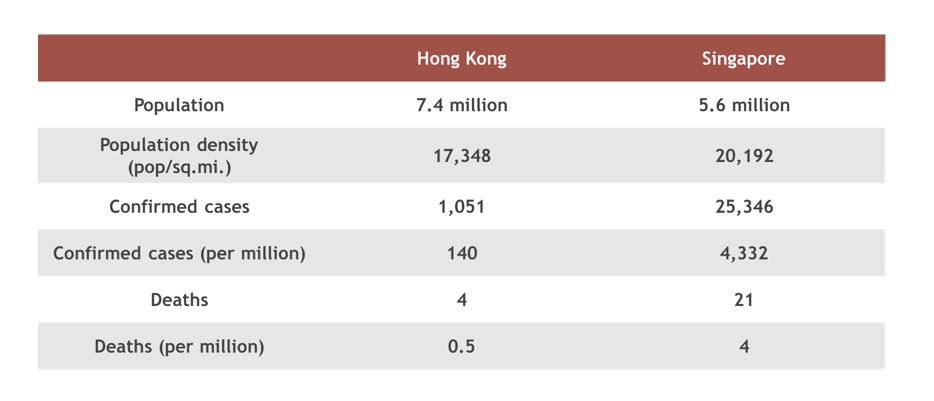

Use of face masks is common practice in high-density populated island-states, such as Hong Kong. Social stigma is attached to those who do not wear facemasks and an ethos of personal responsibility exists. Considering Hong Kong’s geographic proximity to China and population density, it has been remarkably untouched by COIVD-19, with 0.5 deaths for every million people5. Singapore, another Asian island state, has a higher population density and an 8 times higher death rate, possibly due to less prevalent use of facemasks6. Facemasks do not present themselves as a one-stop-shop solution. But if their effectiveness can be properly ascertained, they might present themselves a more viable and cheaper alternative for governments. One estimate suggests the coronavirus lockdown is costing the UK economy £2.4bn a day7. Governments may decide that supplying countries with facemasks and looser restrictions is a more balanced approach. By population density, Hong Kong should have a higher death rate, but undoubtedly social and hygienic practices have helped mitigate this.

If social backlashes make reinforcing lockdowns unfeasible, the governments could begin to place the onus on the more economically friendly method of personal responsibility and social pressure.

Source: Bloomberg, Wikipedia/Smith & Williamson Investment Management LLP, as at 12 May 2020

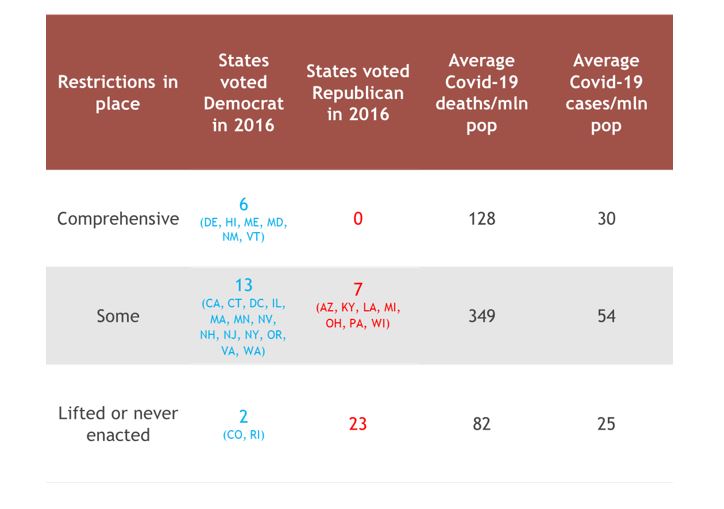

5) US lockdowns have become political

To think that political lines would not be drawn down the middle of a pandemic would have been naive. According to the Wall Street Journal, 6 out of 6 states with comprehensive measures in place voted Democrat in 2016, whilst 23/25 states who have lifted or never enacted measures, voted Republican8.

A cynic might suggest that Democratic states are holding off on lifting restrictions as they help derail President Trump’s quest for re-election. Others might point to the fact that ‘Democrat states’ generally have higher population densities and require tougher measures. States who have lifted or never enacted restrictions have an average COVID-19 death rate of 82 per million people, compared to states with comprehensive restrictions who have 1289. It is thus unlikely that these states will introduce lockdown measures, even given a second wave. Again, this supports the narrative that continued lockdowns may not be implemented across the board. If the US can lockdown on a state by state basis, then it can lockdown on a city by city basis too.

Source: Wall Street Journal/Smith & Williamson Investment Management LLP, as at 12 May 2020

6) Governments are opting for local action

Some governments have already elected for this localised tactic. Germany have introduced a new “emergency brake” as a safeguard against COVID-19. Municipalities with more than 50 new infections per 100,000 over the last 7 days must reimpose some form of restrictions. If the outbreak cannot be traced, then transport will be restricted in and out of the affect area. Limiting travel between areas is essential to localised lockdowns, the aim being to contain virus outbreak areas as tightly as possible.

lsewhere, South Korea recently has been able to trace a spike of infections back to a singular nightclub, whilst China re-imposed lockdown on Jilin City in the north east of the country. By not having to put an entire economy on pause, localised lockdowns look to be much more attractive. Germany is demonstrating local action is a viable and more cost-effective solution. More governments may move in this direction.

To conclude, localised lockdowns are integral to a V-shaped economic recovery and governments may opt in their favour. It is not clear that lockdowns necessarily lead to fewer deaths overall and lifting them has not reignited infection rates in Denmark. They do, however, cause significant economic damage and come at a heavy cost. Social pressure from areas experiencing less impact from COVID-19 may tie politicians’ hands, especially in the US. Meanwhile countries like Germany could lead the way for localised lockdowns as standard to prevent and contain future pandemics.

Given the option, a targeted response to another COVID-19 outbreak may be governments’ best option, economically and politically. A less draconian approach lowers the risk of disruption to a V-shaped economic recovery, seemingly built into equities.

Please note specified government legislation is that prevailing at the time, is subject to change without notice and depends on individual circumstances.

Sources:

- Worldometers/Smith & Williamson Investment Management LLP, as at 12 May 2020

- Bloomberg/Smith & Williamson Investment Management LLP, as at 12 May 2020

- Bloomberg/Smith & Williamson Investment Management LLP, as at 12 May 2020

- Worldometers/Bloomberg/Smith & Williamson Investment Management LLP, as at 12 May 2020

- Bloomberg, Wikipedia/Smith & Williamson Investment Management LLP, as at 12 May 2020

- Bloomberg, Wikipedia/Smith & Williamson Investment Management LLP, as at 12 May 2020

- The Times, https://www.thetimes.co.uk/article/consumer-confidence-at-its-lowest-since-the-financial-crisis-p6phf7x3k, as at 12 May 2020

- Source: Wall Street Journal/Smith & Williamson Investment Management LLP, as at 12 May 2020

- Source: Wall Street Journal/Smith & Williamson Investment Management LLP, as at 12 May 2020

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

RISK WARNING

Capital at risk. The value of investments and the income from them may go down as well as up and investors may not get back the original amount invested. Past performance is not a guide to future performance. Further information is available in the Key Investor Information Document (KIID), the risk section of the Fund’s prospectus and the Fund Factsheet. Please read the KIID before making any investment decision.

Evelyn Partners Investment Management LLP

Authorised and regulated by the Financial Conduct Authority.

Registered in England No. OC 369632. FRN: 580531

Evelyn Partners Investment Management LLP is part of the Evelyn Partners group.

© Evelyn Partners Group Limited 2021

Ref: 72320eb

Return to the COVID-19 homepage